Banks Discriminate Against Legal Gun Sellers as ‘Firearms Dealers’

Blame the Obama Administration's "Operation Choke Point" for targeting legal gun businesses.

The stories of two businessmen who recently were denied banking services because they sell firearms suggest a secretive government program called Operation Choke Point still affects industries across the nation that the Obama administration considered undesirable.

In one case, a large bank in New England denied a line of credit to a former police officer who started a gun and tactical business in Monroe, Conn., saying it “no longer lends to firearms dealers.”

In the other case, a branch of a North Carolina bank refused to set up a new payment service for a firearms seller in Tryon, N.C., because of the nature of his industry, the business owner said.

The Daily Signal talked to both businessmen, who say they are being punished for their line of work despite efforts in Congress to end discrimination by banks against gun sellers.

Some experts believe that banks’ decision not to do business with gun sellers stems from Operation Choke Point, a Justice Department program that, according to government officials, aimed to “attack Internet, telemarketing, mail, and other mass market fraud against consumers, by choking fraudsters’ access to the banking system.”

Critics of the program say it was used to put the financial squeeze on entire industries the Obama administration doesn’t like, such as firearms sellers and payday lenders.

“It is increasingly clear that the effects from Operation Choke Point are continuing to be felt, even if the administration has told Congress it has backed off from this campaign,” Larry Keane, senior vice president and general counsel for the National Shooting Sports Foundation, one of the nation’s leading lobbying firms for the gun industry, told The Daily Signal.

‘It Came Back Denied’

Rich Sprandel, an 18-year police veteran, had to retire in 2011 from the force in Seymour, Conn., after being hit by a drunk driver while on duty in his patrol car. Sprandel, who is married and has two children, opened an online firearms and tactical business.

“I have a retirement pension, but it’s not 100 percent of my pay, so I need to make a living to support my family,” Sprandel, 48, who owns Blue Line Firearms & Tactical in Monroe, Conn., said in an interview with The Daily Signal.

On March 7, he got a voicemail message from a vice president at People’s United Bank in Fairfield, Conn., regarding his request for a new line of credit.

“It came back denied,” the bank official says in the voice message obtained by The Daily Signal. “They said they no longer lend to firearms dealers, so that’s a new thing for us.”

He goes on to tell Sprandel: “I know I’ve done them before where it was the [gun] manufacturers, and it went through without a problem, but they’re not doing it with the dealers, so sorry about that.”

The caller identified himself by a first name matching that of a bank vice president with whom Sprandel said he dealt. The bank officer did not respond to The Daily Signal’s multiple requests for comment.

Sprandel said this is the second time he has been denied financial services because he sells firearms. This time, the retired police officer decided to call on supporters of gun rights to boycott People’s United Bank.

“Why should Second Amendment supporters support a bank that doesn’t support them?” Sprandel said.

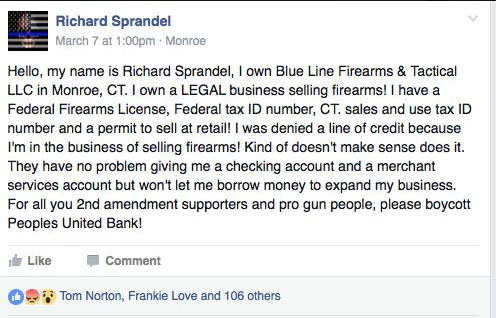

In a Facebook post written on March 7, Sprandel called on Second Amendment supporters to “boycott People’s United Bank” for denying him a line of credit. (Photo: Sprandel/Facebook)

The Daily Signal called and emailed People’s United Bank on multiple occasions to clarify the bank’s position on doing business with Americans in the firearms industry. The bank did not respond.

‘High Risk’ Business

Another firearms dealer, Luke Lichterman, told The Daily Signal that HomeTrust Bank denied banking services to him March 11 because of the “high risk nature” of his business, Hunting and Defense, in Tryon, N.C.

Lichterman, a Columbus resident, said he was trying to open an automatic clearing house payment service with HomeTrust, where he had maintained accounts since 2012.

But, he said, a treasury management sales officer at the Asheville branch of the bank denied his request on March 11 because of his line of work.

“He explained that he’s terribly sorry, but the banking industry is tightly regulated by the federal government and we cannot approve your [payment service] because of the high risk nature of your business,” Lichterman said. “I said, high risk? What risk? What’s the problem?”

Lichterman, 75, said the banker then said, “I’m sure your business is fine, but it’s your industry that we feel is too risky.”

Luke Lichterman, co-owner of Hunting and Defense in Tryon, N.C., said he would like to see the banks “stop censoring” his business. (Photo: Lichterman)

Suspicious of a connection to Operation Choke Point, which the Justice Department launched in 2013, Lichterman asked the banker for another example of an industry that HomeTrust Bank wouldn’t do business with.

His immediate response: “pornography.”

“I really had to stop from laughing,” Lichterman recalled. “I said, I’m not a pornographer. I deal in constitutionally protected goods.”

Stacie Hicks, senior vice president of marketing and public relations at HomeTrust Bank, told The Daily Signal that the bank “does not comment on customer accounts, both to honor their privacy and to comply with federal privacy regulations.”

‘Continuing to See Discrimination’

Keane, the lawyer for the National Shooting Sports Foundation, said the group is “gratified” by House passage in February of HR 766, the Financial Institutions Consumer Protection Act, sponsored by Rep. Blaine Leutkemeyer, R- Mo. The bill was introduced as a direct response to Operation Choke Point.

Keane told The Daily Signal that the group “would urge additional hearings to find out why businesses in our industry are continuing to see discrimination where lenders use wording very similar to that used in Operation Choke Point.”

Operation Choke Point was designed by the Obama administration to fight money laundering by using the Justice Department’s investigatory powers to “choke off” fraudsters’ access to the nation’s banking system. The Justice Department did so by partnering with federal banking regulators who could pressure banks to close the accounts of those in industries they considered “high risk.”

Critics say federal authorities abused their authority under the program by pressuring banks not only to close the accounts of illegal, fraudulent businesses, but also entirely legal industries that the Obama administration doesn’t like.

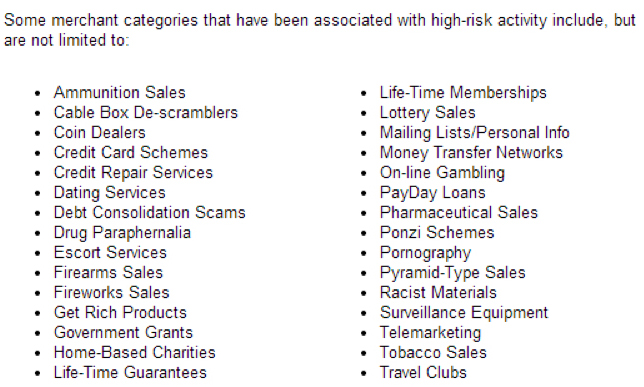

To support these claims, critics cite a 2014 congressional report investigating Operation Choke Point. According to the report, federal agencies sent thousands of U.S. banks formal guidance identifying categories of merchants the agencies considered high risk. That list featured “firearms” and “ammunition” sales, along with “pornography.” Here it is:

According to the congressional report, the Federal Deposit Insurance Corporation (FDIC), which created the list, “explicitly intended its list of ‘high-risk merchants’ to influence banks’ business decisions.”

Although federal agencies have taken corrective actions since coming under congressional investigation over their role in Operation Choke Point, The Daily Signal has not been able to determine that anyone was disciplined or fired, and gun sellers such as Lichterman and Sprandel say they’re still feeling the squeeze.

‘Damage Already Done’

But ending Operation Choke Point — or any of the program’s unintended side effects — is more difficult than lawmakers think, close observers say.

“Even if you stop the program, the damage has already been done,” Brian J. Wise, a senior adviser at U.S. Consumer Coalition, which has raised public awareness about Operation Choke Point, said. Wise added:

The banks and the payment processors already know who is on the hit list from the administration. So whether or not a regulator says, ‘You’re safe now,’ they’re always going to try to de-risk those industries because they don’t want any undue pressure.

Lawmakers attempted to defund the Justice Department program in 2014 and again in 2015, but neither effort proved successful. In February, the House passed the Financial Institutions Consumer Protection Act, which would ban federal agencies that oversee banks from requesting or ordering that banks terminate customer accounts, “unless the regulator has material reason,” but that bill has not yet been taken up by the Senate.

While Wise supports the Financial Institution Customer Protection Act, he said that legislation is unlikely to have any material effect.

“[Lawmakers] said that they were going to produce legislation to stop a program that doesn’t exist — we’re going to cut funding for it,” Wise told The Daily Signal, adding:

Well, guess what? There was no funding appropriated for Operation Choke Point in the first place, so all this is is a PR stunt. If these industries want to stop this program — if American consumers want to stop this program — legislation is not the answer. They have to go to the voting booth and they have to vote out the people that put this program in place in the first place.

Obama Administration Response

The Office of the Comptroller of Currency, the Treasury Department agency responsible for regulating People’s United Bank, denied any involvement in the bank’s decision to deny service to Sprandel.

Agency spokesman Bryan Hubbard said:

The situation you describe appears to be business strategy decisions by individual banks based on risk assessments they perform. As a general matter, the [Office of the Comptroller of Currency] does not direct banks to open, close, or maintain individual accounts or particular customers and has provided no guidance to bankers that would result in the decision to avoid banking an entire industry.

The Federal Reserve, which regulates HomeTrust Bank, did not respond to requests for comment.

In February, the Obama administration made clear its stance against any efforts to restrict banking regulators’ ability to “engage” with those they regulate.

Taking away these capabilities, the White House said in a statement regarding the 2016 bill to end Operation Choke Point, “would constrain federal banking regulators’ ability to appropriately engage with the financial institutions they regulate for compliance with and enforcement of U.S. legal and regulatory requirements that are designed to protect the United States financial system from money laundering, terrorist financing, and other serious financial crimes.”

‘Damage Going On’

When he was denied by People’s United Bank, Sprandel said, he was applying for a $25,000 line of credit so he could move to a larger retail location.

“I was also going to use the line of credit for more inventory once I secured a new location,” he said.

Rich Sprandel owns Blue Line Firearms & Tactical in Monroe, Conn., which sells to law enforcement, competitive shooters, hunters, and those interested in self-defense and home defense. (Photo: Rich Sprandel/Blue Line Firearms & Tactical)

Living in Southwestern Connecticut, where the 2012 Sandy Hook Elementary School shooting is still fresh in people’s minds, Sprandel said, he believes his situation is “probably a combination” of government regulation and private banking decisions.

Four days after applying, Sprandel was able to obtain a line of credit from Wells Fargo without issue. But that doesn’t stop the former police officer, who now sells firearms and accessories to local law enforcement agencies, from feeling “snubbed.”

“They’re discriminating against me because of what I sell,” Sprandel said. “I have a legal business. I’m not selling marijuana illegally. I have a legal, federally regulated business.”

Lichterman, the second firearms dealer, said his bank’s rejection of his request continues to hurt his ability to do business.

“If I were doing [an automatic clearing house payment service], there’s a monthly fee — $25 a month and 10 cents a charge,” he said.

Instead, Lichterman must take payments by credit card, which costs him 4.5 percent of each payment.

For example, he said: “This morning, I’m processing two orders at about $1,500 each; [at] 4.5 percent you’re looking at $70, more or less. Doing it through the bank, $25 for the monthly fee and 10 cents a charge, you see the difference — it’s big.

“There’s damage going on but, hey, we gotta do it,” Lichterman said. “We’ve got an election coming and hopefully some of this stuff will change.”

Copyright 2016 The Daily Signal